The Financial Reset Every Woman Needs

Frugal Chic® #48: the financial literacy guide I wish I had at 18

Happy Sunday!!

It’s a new financial year, so for us at Frugal Chic®, it matters even more than January.

This is the time to reset, assess where you are now, and look at what you can optimise going forward.

One thing I’m still not happy about is the gap in financial literacy, particularly among women. Boring Money’s 2025 estimate puts the UK gender investment gap at £678 billion1. It’s safe to say we need more women to care about their finances, feel that it’s for them and to close the knowledge gap. This is something I’ve always tried to change through my content by being transparent about money, breaking down complex ideas into simple frameworks, and representing a different kind of image in the finance space.

Like many people, I spent years trying to look the part. I wanted to look like I had everything together: the right clothes, the right makeup, the right skincare. I thought that would make me feel liked and accepted. What I did not realise was that building financial freedom would become the single biggest factor in the confidence and freedom I have now. Being able to work for myself, increase my income, and rely on an emergency fund has given me more confidence than any blush or cleanser ever could.

So, in this issue, I want to go back to basics. Not in a patronising way where I compare stocks to lip gloss, but in a practical one, the money handbook I wish I had at 18. Because every new financial year is a chance to get honest about where you are, unlearn what is not serving you, and build better systems from there. This was inspired by my ultimate role model Devamsha @ Financial Hot Girl, she has been my goat for content since day 1 and this newsletter wouldn’t exist without her influence on me.

(Not financial advice. When investing, your capital is at risk. This is purely for informational purposes only.)

in this issue:

the money stories and limiting beliefs shaping how you earn, spend, save, and invest

a money audit to get honest about where your finances stand right now

how to save properly, so it feels intentional rather than restrictive

investing basics, so you can build long-term wealth with more clarity and less fear

the key tax allowances and optimisation opportunities worth knowing this financial year

how to approach debt and credit cards without shame, and manage them more strategically

simple systems and automations that make good money habits easier to maintain

the money stories you need to outgrow

The first thing I want you to recognise is that there is no such thing as being naturally ‘bad with money’. Money is a skill. It is something you learn through exposure, through trial and error, and through being in environments where these conversations are normal. Some people obviously have a massive head start.

I did not go to private school. My parents were not financially literate, and I did not grow up around many people who understood how money worked. So, like a lot of people, I spent my early years navigating money in the dark.

Honestly, it was almost by chance that when I got to university, I had male friends who talked about stocks as casually as they talked about beer or football. That was when these conversations started to open up for me. But at the beginning, I was very much pretending I knew what an ISA was and clumsily pronouncing it ‘I-S-A’ instead of ‘Ice-ah’.

While I was curious to learn and took it upon myself to self-study the topic for 7+ years, I realised through trial and error, and learning the hard way, that a lot of unhelpful beliefs were still directing my money choices.

I remember being deep in my shopaholic phase and saying things like, “I’m too broke right now,” “I can’t afford that,” or “I’m so bad with money,” as if it were a badge of honour, a self-deprecating joke. And in the UK, we do love a bit of that.

And that is the thing. A lot of people are moving through adulthood repeating inherited beliefs without ever questioning whether those beliefs are useful.

Things like:

I’m just bad with money

wanting more money is greedy

hard work will make you rich

money is either for spending now or saving for later

If you believe money is ethically wrong, you are less likely to ask for more, earn more, invest more, or build more. If you believe hard work should automatically equal income, you will be confused by a world that rewards leverage, ownership, and scalability over effort. If you think about money dogmatically, as though it only has one job, you end up living a restrictive life at both ends of the frugal and frivolous spectrum.

These kinds of beliefs are not especially helpful for building wealth because they are often rooted in scarcity, shame, or simply not knowing any better. The goal isn’t to judge yourself for having them, but to reflect on whether they are truly helpful to your financial life right now.

Frugal Chic® Tip: The next time you catch yourself saying something about your relationship with money, ask yourself, do you genuinely believe that or have you inherited that view?

your financial reality check

Before you start following a complicated budget, paying off debt, or investing, there’s one simple step you can take to get on the path to clearer finances: a money audit.

It’s an honest look at where you currently are financially.

Grab a pen and paper and sit down, note:

your income

your expenses

your savings

your pension

your investments

your debt

The reason this matters is because, without a clear picture of where you are, all your goals stay vague.

You end up saying things like, “I want to save more this year,” instead of, “I have £180 left after my fixed and variable expenses, so I can realistically direct that towards my emergency fund.”

Once everything is laid out, organise your expenses into fixed, variable, and one-off categories. Add them up. Then subtract your monthly spending from your monthly net income.

E.g. Tallying up your income and it comes to £2,500, your expenses come to £2,135. You then have £365 left over.

That will tell you one of three things:

you have a surplus

you are breaking even

you are in a deficit

If you have a surplus, that is your capacity to save, invest, or accelerate debt repayment.

If you are breaking even, that tells you there is currently no margin for wealth building.

If you are in a deficit, something needs to change, whether that is spending, income, or both.

If you are the last two, that is totally normal and this is not a judgement. However, just doing this simple act gets you closer to where you want to be. Forget about age, comparison, expectation, this is simply your own relationship with money that you’re getting more honest about.

The benefit of doing this is to clearly see everything in one place rather than fragmented through bank accounts, budgeting apps, and emails.

The next step is to ask yourself:

Does my spending reflect the life I actually want to build?

Where am I overspending out of habit, convenience, boredom, or emotion?

Where am I being too restrictive in ways that make life feel unnecessarily joyless?

Are my purchases supporting a chosen identity, or are they trying to manufacture one?

A lot of spending is not about the item itself. It is about what the item represents. Status. Comfort. Distraction. Belonging. Having this awareness allows you to make more intentional choices later on.

Frugal Chic® Tip: Make a splurge vs save list: things you love spending on and things you don’t.

Rather than saying “I want to save more” or “spend less”, you know what you’re working towards, which is pouring into those areas you value.

saving is the real self care

The first golden rule of personal finance is simple: you must spend less than you earn. If you do not do that, you cannot save. And if you cannot save, you cannot build wealth. There is no way around this. But just because it’s a simple rule, it doesn’t mean it’s easy. If it were easy, Buy Now Pay Later companies wouldn’t thrive. That’s why it’s kinda unhelpful to tell people they should save, we all know we ought to do that, so instead let’s get into the mind of a saver, see how they think differently.

There are people who save consistently do not view it as punishment or restriction on their current life.

Instead of treating saving like an unpleasant chore or something they “ought” to do, like eating the veg on their plate or going to the dentist, they treat it as a strategic decision about what they want their life to look like in five, ten, or twenty years.

Who save effortlessly aren’t magically born better at managing money, they simply have values as established with the Splurge vs Save list, and they use systems like a clear budget.

A common rule of thumb is the 50/30/20 budget2. The idea is simple: allocate 50% of your after-tax income to needs, 30% to wants, and 20% to savings or debt repayment.

In practice, in cities like London or New York, it is often unrealistic.

When rent alone can take up 40–50% of take-home pay, expecting all essential living costs to fit neatly into the remaining margin can feel restrictive. The result is that many people feel they are “failing” at budgeting, when in reality the framework no longer matches modern economics.

I’ve come up with a more realistic version, which I call the Frugal Chic 4 C’s. We divide our after-tax income into: Core, Cushion, Compound, and Curate.

Core - 60%: essentials like rent and bills

Cushion - 10%: emergency fund

Compound - 20%: pensions, ISAs - where real wealth is built

Curate - 10%: fun money pot

Due to the values of Frugal Chic® which is to optimise for freedom and optionality, the compound bucket is perhaps larger than what other budgeting frameworks show. You can adjust it to your liking.

It’s also worth noting that your cushion (emergency fund) will inevitably fill up, which means you could allocate that extra 10% to your Curate fund.

The purpose of the 4 C’s is not to fit your finances perfectly into the percentages but to have a reference point, a guideline. Don’t worry if your Core is coming to more than 70% and you physically can’t save at the moment. This guide is simply to bring awareness at this stage.

invest with confidence

Investing is often the most daunting topic when it comes to personal finance. I remember feeling like it was akin to gambling, or that you had to be an expert. This section aims to demystify it and simplify it, showing that investing can be simple, accessible, and one of the most powerful tools for creating long-term freedom.

It really can be broken down into a few steps:

start with active research: a podcast on a walk, a youtube video in the evening, a money book for the month

build your cushion first: 3-6 months worth of living expenses, it ensures you don’t have to potentially sell during a downturn (essential in times like these)

understand the time horizon: don’t invest money you might need in the next 5 years

choose the right account wrapper: in the UK that’s an ISA, pension etc.

keep it simple: For many beginners, one low-cost global index fund is enough to start.

automate it: Set up regular contributions and let consistency do its job.

The key thing to remember is you do not need to feel like an expert to begin. You need to understand enough to act responsibly, then stay consistent long enough for compounding to work it’s magic.

Compound interest is when you earn interest on both your original money and the interest already added.

Example:

You invest £1,000 and earn 10% a year.

Year 1: you earn £100 → total £1,100

Year 2: you earn 10% on £1,100, not just the original £1,000 → £110

Year 3: you earn 10% on £1,210 → £121

That is compound interest.

With stocks though, you are not usually being paid “interest” in the normal sense. Your money is growing through returns.

Compound interest is a type of compounding, but investing is more accurately driven by compounding returns.

it’s not about how much you earn, it’s how much you keep

One of the biggest expenses of our time isn’t a fancy car or luxury holiday, it’s tax. We’re taxed pretty much at any stage of life, when we work, buy things, even (god forbid) die. So Frugal Chic® women know that legally avoiding overpaying it is the smart move.

You do not need to become a tax expert overnight, but you should know the key allowances available to you so you are not accidentally leaving money on the table.

More specifically, here are a few key ones for the UK for 2026/27.

ISA allowance

You can put up to £20,000 across your adult ISAs in the 2026 to 2027 tax year, and the tax year runs from 6 April to 5 April. A Lifetime ISA still has a £4,000 annual limit within that overall ISA allowance. You could consider opening an ISA with XTB who are offering 6% on a Cash ISA currently for the first 90 days after opening.

AD | Disclaimer: Your capital is at risk when investing. The value of investments and the income from them can fall as well as rise and you might lose the original amount invested. Fluctuations in such value and income can result from factors such as market movements and variations in exchange rates. Past performance is not a reliable indicator of future results. 2% ISA rate boost for 90 days. New clients only. T&Cs apply.

Pension annual allowance

The standard pension annual allowance is £60,000. This can be lower for some higher earners because of tapering, and the tapered annual allowance floor remains £10,000.Trading allowance

You can earn up to £1,000 in gross trading or side hustle income each tax year before you may need to report it, although there are exceptions depending on your wider tax situation.

If you want to use this new financial year properly, the aim is not to max out these allowances - very few people are able to do that. But knowing about them and taking small steps towards using them is the key.

debt is not a personality flaw

That is one of those topics that brings up a lot of shame in people, but it really shouldn’t be that way. Debt is not a failure. It is often the result of poor education, aggressive marketing, survival decisions, low income, or simply not understanding how it works. Notice how none of those options were frivolous or putting the blame on you.

Credit is also pushed onto us constantly. It used to be mostly credit cards. Now it arrives rebranded as Buy Now Pay Later services. Klarna. Clearpay. Instalments. Tiny decisions that do not feel like debt until they ultimately do.

The issue with debt is not only the balance. It is the feeling. Owing your future income to someone else is one of the worst financial feelings there is.

So, I personally haven’t been in debt because my parents told me credit cards were evil, but if I had been in debt, this is exactly what I would do.

So the first step is clarity.

List every debt:

lender

balance

minimum payment

annual interest rate

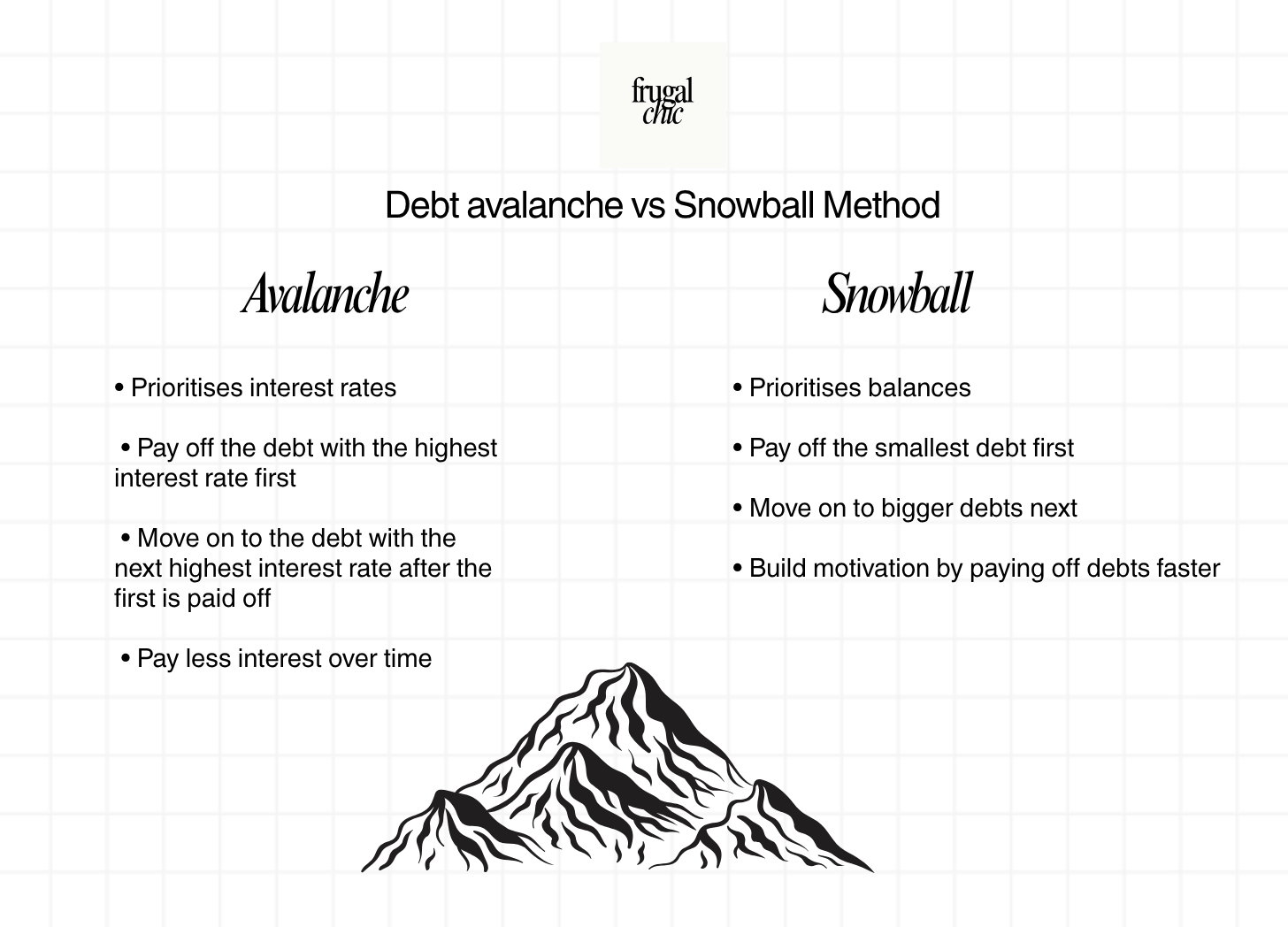

Then choose a repayment method.

Debt avalanche means paying off the highest-interest debt first. It is mathematically most efficient.

Debt snowball means paying off the smallest balance first. It is not always the cheapest, but it can be better for motivation.

If you have high-interest consumer debt, tackling that is often a better financial move than rushing to invest. A credit card charging punishing interest is likely doing more damage than your investments can undo.

This won’t happen overnight, but knowing about these methods and putting a name to them can make you feel like you’re one step closer to clearing it.

automate the boring

Often we ignore finances because they feel like one of those obligatory life admin tasks that just saps the life out of us.

But often, not looking at these things makes your life a whole lot more chaotic. So if your whole financial life depends on remembering, deciding, resisting, or manually moving your money around every month, eventually it will be one of those extra things that sets you over the edge on a really busy day.

You have limited energy, and while the rest of this letter was about saving money, saving your energy and time are just as important.

So automation speeds up this process and puts your saving on autopilot.

I would aim to set up automations for all of these different buckets:

your bills

your savings

your investments

your spending money

Something that I did only recently, which I am quite embarrassed to admit, is set up the direct debit to my partner’s bank account because we split our rent and bills 50/50. It only made sense for me to set that up exactly on the day I get paid because before, I was remembering, setting a calendar notification, and manually transferring it, and it was just another thing that I had to do, especially as someone trying to run a business.

Automating also allows you to plan ahead for big spending goals. If you know your yoga class costs £12 a week, build that into your Curate bucket. If you know Christmas always catches you off guard, even though it happens every single year like clockwork, set up the sinking fund now and spare yourself the annual suprise to your finances.

So, having systems and automations in place just makes saving and investing an automatic part of your life and identity rather than something that you actively have to try and force yourself to do.

redefining wealth

I saw a quote from Erin Confortini, who is one of my favourite creators on money, and she said:

“I don’t want to be rich, I want to be free, but in order to be free I have to be rich,”

That really stuck with me because that is ultimately my goal with financial literacy and financial freedom: to understand these things closely, not to obsess over money, but to understand what money can buy, which is more time, optionality, and freedom.

Once you have control of your money, you notice how it stops controlling your mood, your choices, and your sense of self. It’s there to build stability and structure so that you’re not constantly swayed by marketing or impulse spending, but rather you spend intentionally on the things you truly value.

In my last letter, I talked about low status, high income, and how a lot of people are optimising for high status but with fragile financial backing. In this new era of AI, geopolitical uncertainty, I think it is even more important now than ever to focus more on building true wealth that is meaningful to you rather than what looks good to society.

So now you’ve read this newsletter, I hope you feel one step closer to being more financially literate. The point isn’t to be perfect or to try and do this all overnight. It’s simply to understand that these steps can be broken down very simply. You do not necessarily have to read a whole book or watch endless YouTube videos. You can start today with small habits.

Until next week,

Mia

https://www.boringmoneybusiness.co.uk/learn/articles/the-gender-investment-gap-increases-for-second-year-in-a-row/

50/30/20 was popularised by U.S. Senator and bankruptcy expert Elizabeth Warren and her daughter, Amelia Warren Tyagi, in their 2005 book All Your Worth: The Ultimate Lifetime Money Plan.

You explained things in a very simple way and it feels inspirational to hear that many of our behaviors around money are actually inherited and influenced by our surroundings.

Great article and thanks for the motivation boost to change mindset first!

Keep this education going! My parents recently got divorced and my dad handled all of the finances, as that was his line of work. But I now sadly see my mom so baffled when it comes to managing all of this. Things like home insurance, car insurance, and property taxes are all so confusing for her. I’m a finance major, so I’m happy to help her, but I start thinking, how many other women out there are just like her?